- What Is Systemic Financial Risk?

- How Liquidity Cycles Drive Systemic Risk

- Key Causes of Systemic Financial Risk

- Real-World Examples of Systemic Financial Risk

- How Systemic Risk Is Measured

- Early Warning Signs Investors Should Watch

- Impact of Systemic Risk on Different Asset Classes

- Role of Central Banks and Regulation

- Systemic Financial Risk in 2026 and Beyond

- How Investors Can Manage Systemic Financial Risk

- Frequently Asked Questions

- Putting It All Together

Systemic financial risk is the kind of danger that doesn’t announce itself. It builds quietly, in balance sheets and credit flows, until it’s too late to ignore.

Let me walk you through the process of understanding it. what it is, what causes it, and why it still matters in 2026.

I’ve spent years studying how liquidity stress builds before market headlines catch up. Systemic financial risk rarely starts with panic. It starts with structural imbalance.

What Is Systemic Financial Risk?

Let’s start with the basics.

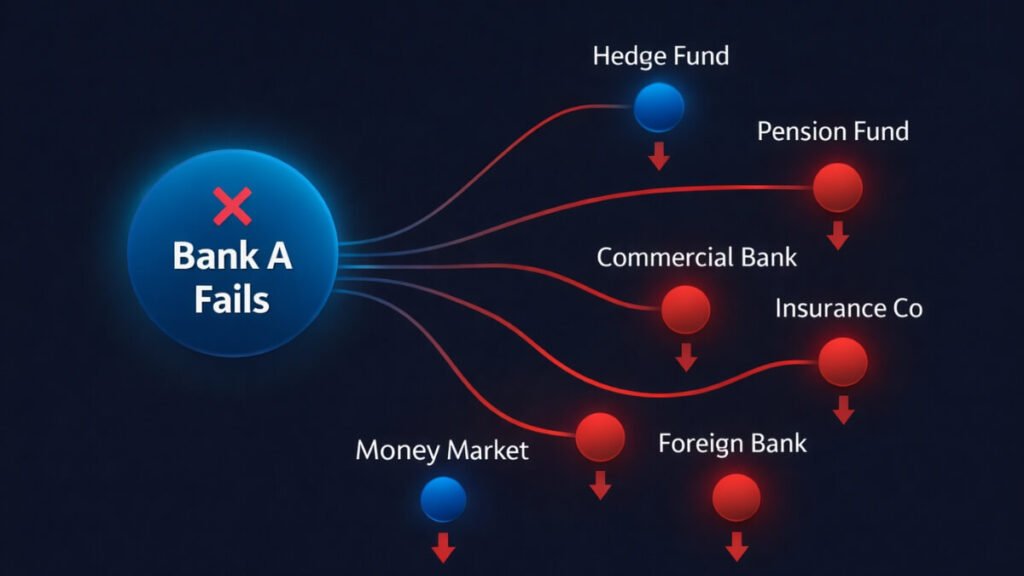

Systemic financial risk is the threat that one failing institution, or a cluster of failing ones, drags down the entire financial system with it. It’s not a single bank losing money. It’s a chain reaction that freezes credit, crashes markets, and hits the real economy.

Academic definitions describe it as the probability that a shock to one node in the financial network spreads to all others. The Bank for International Settlements calls it a disruption to financial services that causes serious negative consequences for the broader economy.

The everyday version: one domino falls, and the whole row goes down.

Systemic Risk vs Systematic Risk

These two sound alike. They’re very different.

| Term | Meaning | Example |

|---|---|---|

| Systemic Risk | Collapse of the financial system due to interconnected failures | Lehman Brothers 2008 |

| Systematic Risk | Market-wide risk that affects all assets at once | Inflation, recessions |

Systematic risk hits your portfolio evenly. Systemic financial risk can hit the whole economy.

How Liquidity Cycles Drive Systemic Risk

Let’s take this step by step.

Expansion, Excess, and Collapse

Financial liquidity is how easily money moves through the system. Banks lend. Businesses borrow. Credit grows.

During expansion, everything looks healthy. Credit is cheap, asset prices rise, and leverage builds quietly in the background.

Then something shifts — a rate hike, a shock, a debt default. Lenders pull back. Credit tightens. The same leverage that looked like smart financing now becomes a weight that pulls firms underwater.

The contraction phase is where systemic financial risk becomes visible. Banks stop trusting each other. Interbank lending dries up. Liquidity disappears from markets that used to have it every day.

Central banks step in. They cut rates. They buy assets. They try to stop the freeze.

But if the imbalance is large enough, intervention only slows things. It doesn’t reverse them overnight.

Key Causes of Systemic Financial Risk

But the causes don’t start with the crash. They start years before.

What Sets It Off

Excessive leverage is almost always in the story. When banks, hedge funds, or households borrow far more than they can repay, a small loss becomes a catastrophic one.

Interconnected financial institutions mean that one firm’s collapse lands on every counterparty’s books. The failure isn’t contained. It radiates.

- Asset bubbles inflate on cheap credit and optimism, then deflate fast when sentiment turns

- Shadow banking (non-bank lenders, money market funds, hedge funds) operates outside standard regulatory checks

- Derivatives exposure creates invisible chains of obligation between firms that look unrelated

- Regulatory gaps let risk build in the corners that regulators aren’t watching

- Cross-border capital flows can reverse suddenly, pulling liquidity out of entire economies at once

The 2008 crisis had most of these. So did the European sovereign debt crisis. They never arrive with just one cause.

Real-World Examples of Systemic Financial Risk

When It Actually Happened

2008 Global Financial Crisis

The subprime mortgage market was the trigger. But the real fuel was leverage. US housing prices had risen by over 100% between 1997 and 2006, fueled by low rates and loose lending. FDIC Crisis and Response

When Lehman Brothers collapsed in September 2008, it wasn’t just a bank failure. Lehman had counterparty relationships across hundreds of institutions globally. Its failure froze the commercial paper market, the repo market, and interbank lending simultaneously. The S&P 500 fell over 56% from its October 2007 peak to its March 2009 trough.

That is the contagion effect. One institution’s insolvency becomes the system’s crisis.

European Sovereign Debt Crisis (2010–2012)

Greece’s debt-to-GDP ratio hit 127% in 2009. Investors panicked. Spreads on Greek, Italian, and Spanish government bonds exploded. Banks holding those bonds saw their balance sheets deteriorate fast.

The fear was that a sovereign default would detonate losses across European banks, which would then stop lending to businesses, which would tip economies into recession. The European Central Bank’s intervention in 2012 — “whatever it takes,” said Mario Draghi — stopped the spiral.

COVID Liquidity Shock (March 2020)

In March 2020, even US Treasury markets, considered the safest in the world, saw liquidity evaporate for a few days. Fund managers needed cash. They sold Treasuries. Prices moved in ways they weren’t supposed to.

The Federal Reserve stepped in with massive asset purchases. Without that, the systemic financial risk from a global shutdown could have triggered a credit freeze worse than 2008.

How Systemic Risk Is Measured

Competitors mostly skip this depth. This is where the real analysis starts.

The Tools Analysts Use

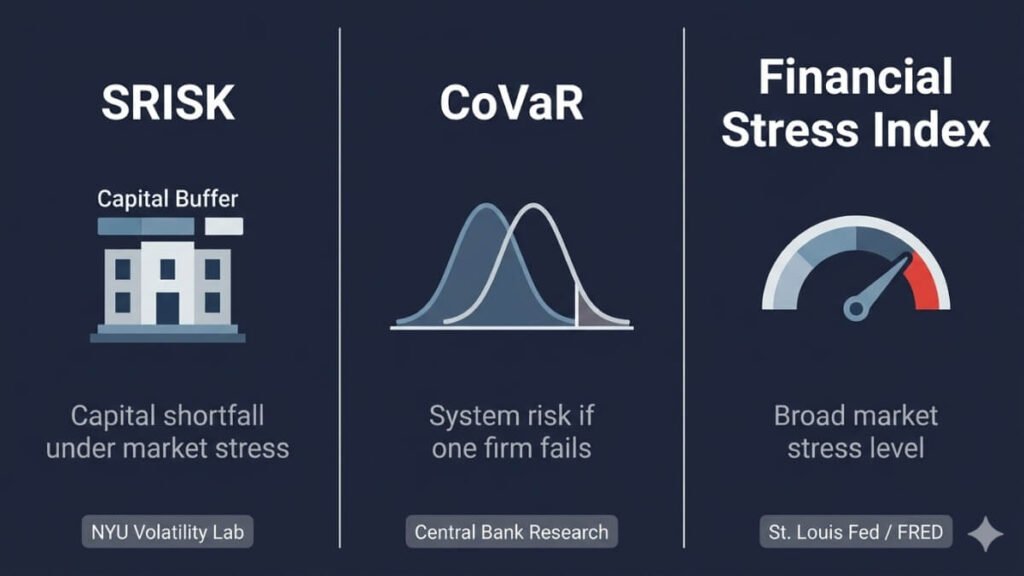

Actually, the number that matters most isn’t one single figure. Analysts use several overlapping indicators.

SRISK measures how much capital a financial institution would need in a market crisis. It accounts for size, leverage, and correlation with the broader market.

CoVaR (Conditional Value at Risk) measures the risk of the whole financial system conditional on one institution being in distress. It was developed by Tobias Adrian and Markus Brunnermeier, and is now widely used in central bank stress frameworks.

Financial Stress Index aggregates signals across credit markets, equity markets, and funding markets into a single score. The St. Louis Fed publishes its own version publicly.

| Indicator | What It Measures | Where to Find It |

|---|---|---|

| SRISK | Capital shortfall under stress | NYU Volatility Lab |

| CoVaR | System risk from one firm failing | Academic / central bank research |

| Financial Stress Index | Broad market stress level | St. Louis Fed (FRED) |

| Credit Spreads | Default risk in corporate bonds | Bloomberg, FRED |

| Yield Curve | Recession probability signal | US Treasury / RBI data |

Credit spreads and yield curve inversions are less precise but more visible. When the difference between corporate bond yields and government bond yields blows out, the market is pricing in higher default risk. When the yield curve inverts (short rates above long rates), recession risk rises.

Early Warning Signs Investors Should Watch

Reading the Warning Signals

Rapid credit growth that outpaces economic growth is usually the first signal. Think of it like a slow leak in a dam. The pressure builds where no one is looking.

Here’s what to track if you want to stay ahead of the cycle:

- Credit growth above GDP growth for two or more years running — this is the classic early signal the Bank for International Settlements has documented across multiple crises

- Rising credit spreads on investment-grade bonds, not just high-yield

- Banking sector stocks underperforming the broader market for several months

- Liquidity drying up in bond markets — bid-ask spreads widen, trade sizes shrink

- Volatility spikes across unrelated asset classes at the same time — this signals correlation breakdown

The last one feels counterintuitive, but it’s actually important. When gold, bonds, and stocks all sell off together, someone is raising cash. That’s a liquidity event, not just a sector rotation.

Impact of Systemic Risk on Different Asset Classes

What Breaks First

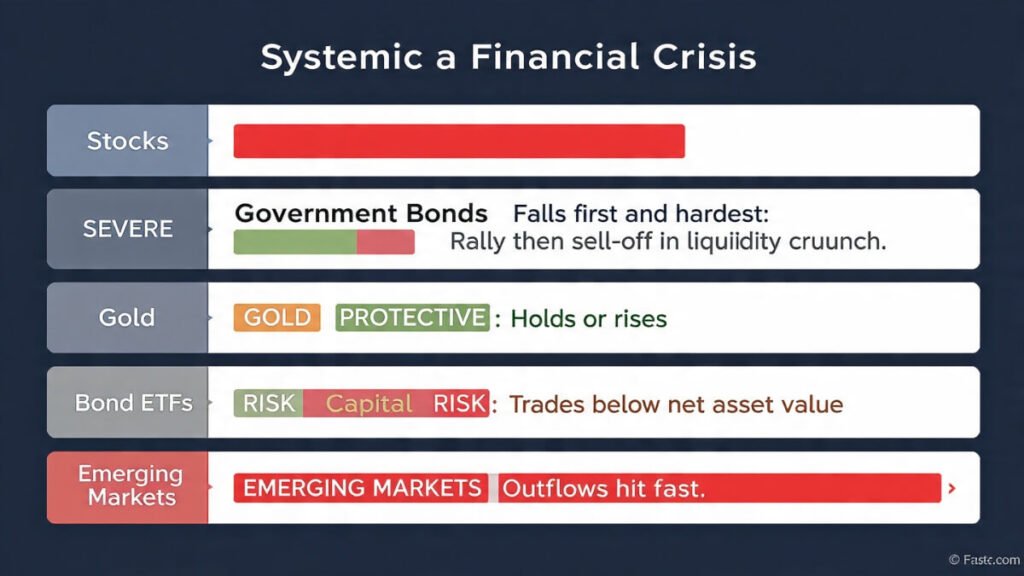

Stocks take the most visible hit. The S&P 500 fell over 56% in 2008–2009. Cyclical sectors — financials, industrials, consumer discretionary — fall first and hardest.

Bonds are more complicated. Government bonds in safe-haven markets (US Treasuries, German Bunds) often rally initially as investors flee to safety. But in the early days of a shock, even they can sell off as investors raise cash (as seen briefly in March 2020).

Gold typically holds up or rises during systemic stress. It’s not guaranteed, but the 2008 data shows gold bottomed out before equities and recovered faster.

ETFs carry a risk most retail investors don’t think about. When the underlying bonds in a bond ETF become illiquid, the ETF itself can trade at a discount to its net asset value. That gap can be severe during a systemic event.

Emerging markets get hit fast by capital outflows. When global investors go risk-off, they pull money from developing economies first. The rupee, the rand, and other EM currencies fell sharply in both 2008 and March 2020.

Role of Central Banks and Regulation

How the System Protects Itself

Capital adequacy requirements under the Basel III framework require large banks to hold a minimum level of high-quality capital relative to their risk-weighted assets. This acts as a buffer against losses. BIS Basel III summary

Stress testing forces major banks to show regulators how they would survive a severe economic shock. The US Federal Reserve’s annual stress tests (DFAST) have become a standard tool post-2008.

Macroprudential regulation focuses on the system as a whole, not individual institutions. Tools include countercyclical capital buffers (raising capital requirements when credit grows too fast) and loan-to-value caps on mortgages.

Quantitative easing allows central banks to buy assets directly, injecting liquidity into frozen markets. The Fed’s QE programs in 2008, 2020, and beyond have all been responses to systemic financial risk events.

Dodd-Frank (2010) was the US regulatory response to 2008. It created the Financial Stability Oversight Council (FSOC) to monitor systemic risks across the entire financial system, not just banks.

Systemic Financial Risk in 2026 and Beyond

What’s Different Now

High global debt levels are the baseline concern. Global debt-to-GDP crossed 350% in 2023 according to the IMF. That leaves the system with less room to absorb shocks than before.

AI-driven trading concentration is a new factor. A small number of algorithmic systems now account for a significant share of daily equity volume. If they all respond to the same signal the same way, it can amplify a market move from a correction into a cascade.

ETF liquidity mismatch is real and underappreciated. Fixed-income ETFs promise daily liquidity on bonds that trade infrequently. In a systemic event, that mismatch can become a problem.

Geopolitical fragmentation is shifting how capital flows globally. Trade restrictions, sanctions, and supply chain rewiring create new vulnerabilities that don’t fit neatly into pre-2020 risk models.

Digital finance interconnectedness adds another layer. Stablecoin platforms, crypto lending protocols, and fintech lenders are now large enough that stress in one corner of digital finance can spill into traditional markets.

How Investors Can Manage Systemic Financial Risk

Practical Steps That Actually Help

Your financial health matters, and the goal here isn’t to predict every crisis. The goal is to build a portfolio that survives one.

Long-term planning pays off. You remain in control when you build in a safety buffer before the stress arrives.

Diversification strategy: Hold across asset classes, geographies, and sectors. Diversification doesn’t prevent loss. It limits concentration when one node in the system fails.

Defensive allocation: Increase exposure to cash, short-duration bonds, and quality companies with low debt when early warning signals start appearing.

Liquidity buffer: Keep 6–12 months of expenses in liquid assets. During a systemic event, illiquid assets cannot be sold at fair value.

Gold or safe-haven exposure: A 5–10% allocation to gold or other safe havens provides partial insulation during correlated market selloffs.

Avoid excessive leverage: This is the most controllable risk. If you’re borrowing to invest, a 30% market drop can wipe out an equity position entirely.

Monitor macro indicators: Credit spreads, the yield curve, and interbank lending rates are publicly available. Knowledge empowers decisions. Watching them takes 15 minutes a month.

Frequently Asked Questions

What is systemic financial risk?

Systemic financial risk is the possibility that the failure of one or a few financial institutions or markets triggers a collapse across the entire financial system. It’s driven by interconnectedness, excessive leverage, and contagion effects. The 2008 Global Financial Crisis is the most studied example.

What causes systemic financial crises?

The most common triggers are excessive leverage, asset bubbles, interconnected institutions, and regulatory gaps. No single factor causes a crisis. They almost always combine — cheap credit fuels a bubble, leverage amplifies losses, and interconnectedness spreads them.

How is systemic risk different from systematic risk?

Systemic risk refers to collapse of the financial system due to linked failures. Systematic risk (market risk) is the broad risk affecting all investments, like inflation or recessions. Systematic risk is diversifiable only in a limited sense. Systemic risk affects the whole system at once.

Can systemic risk be predicted?

Not precisely. But early warning signals are well-established. Rapid credit growth above GDP, rising credit spreads, banking sector weakness, and yield curve inversions have preceded most major crises over the past 50 years. The timing is uncertain. The buildup is usually visible.

How do central banks prevent systemic collapse?

Central banks use stress testing, capital adequacy rules, macroprudential oversight, and emergency asset purchases. The Fed bought over $1 trillion in assets in the first three weeks after COVID hit in March 2020. Speed and scale of intervention are now understood to be critical.

What is SRISK and why does it matter?

SRISK is a measure of how much capital a financial firm would need if global equity markets fell by 40% over six months. It’s calculated by the NYU Volatility Lab and is used by central banks to identify which institutions pose the greatest threat to financial stability if they run into trouble.

Putting It All Together

Systemic financial risk is not an abstract concept for economists. It’s a real force that determines whether the credit in your bank account stays accessible, whether your employer can roll over its business loans, and whether the pension fund holding your retirement savings survives a crisis intact.

Watch the signals. Build the buffer. Knowledge empowers decisions — and in finance, early awareness is the only edge most investors will ever have.

About Sanjay: Financial risk analyst specializing in liquidity cycles and systemic stability. Writes on macro-financial risk signals, credit cycle analysis, and global financial market dynamics.